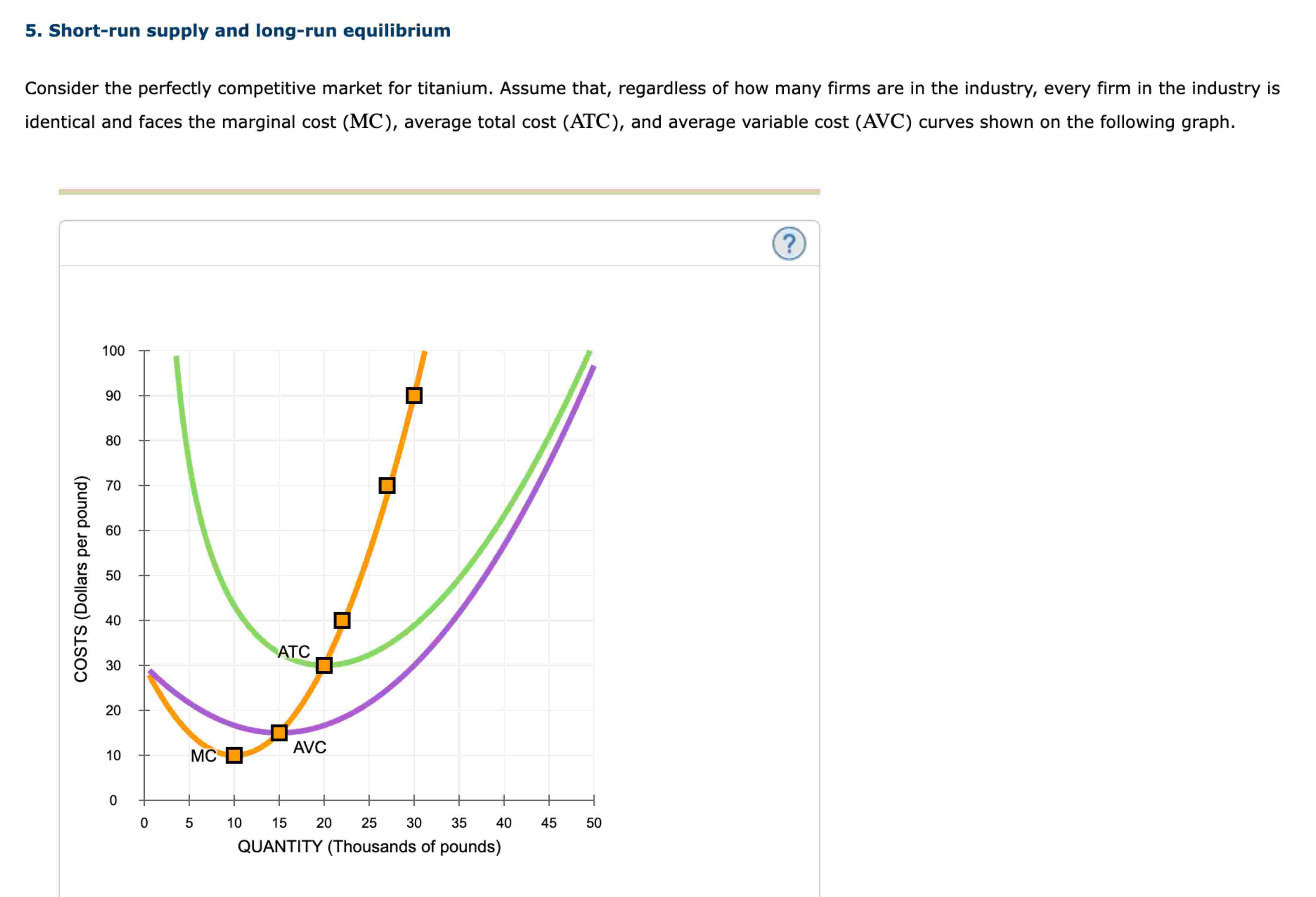

(Solved): 5. Short-run supply and long-run equilibrium Consider the perfectly competitive market for titanium ...

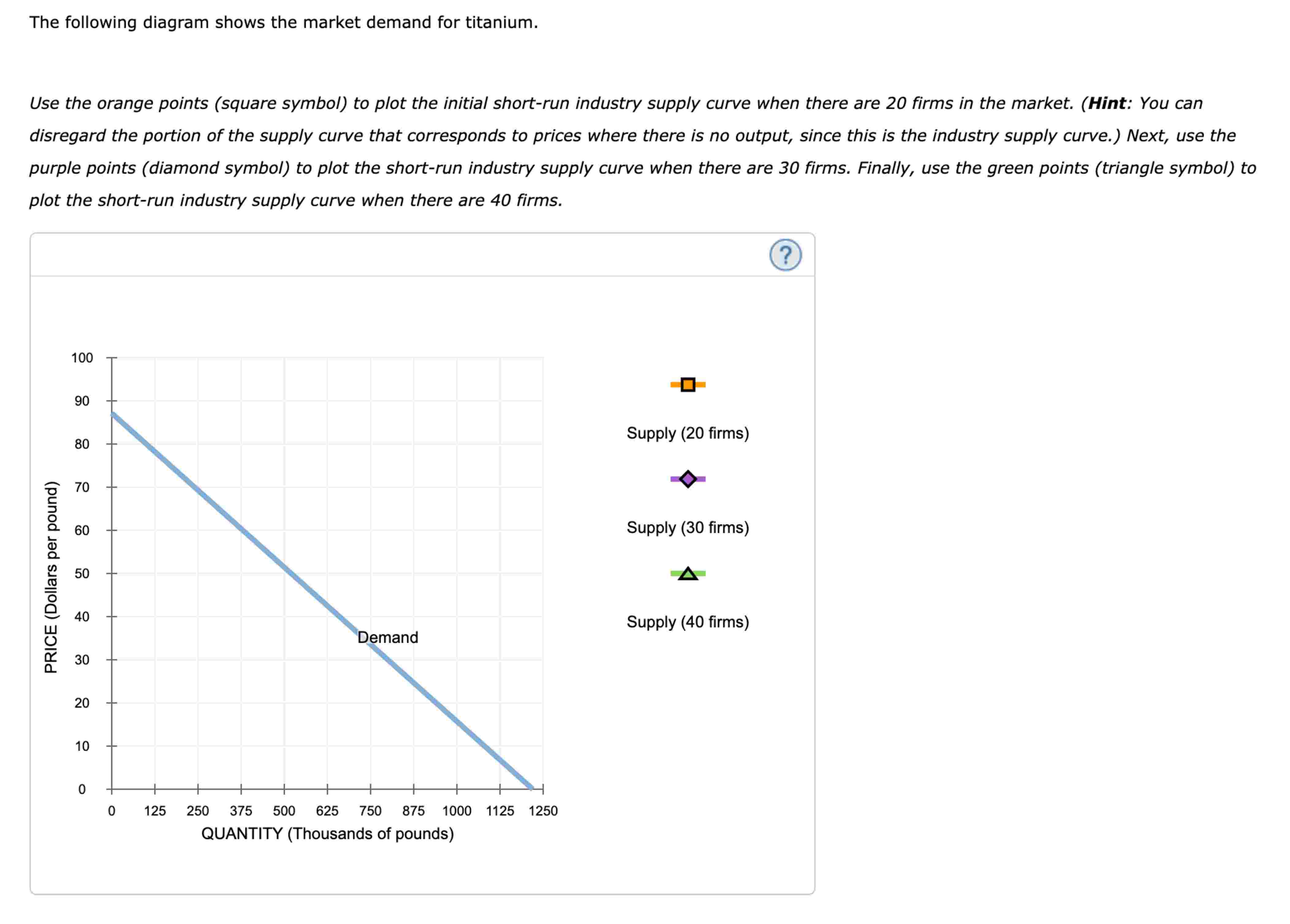

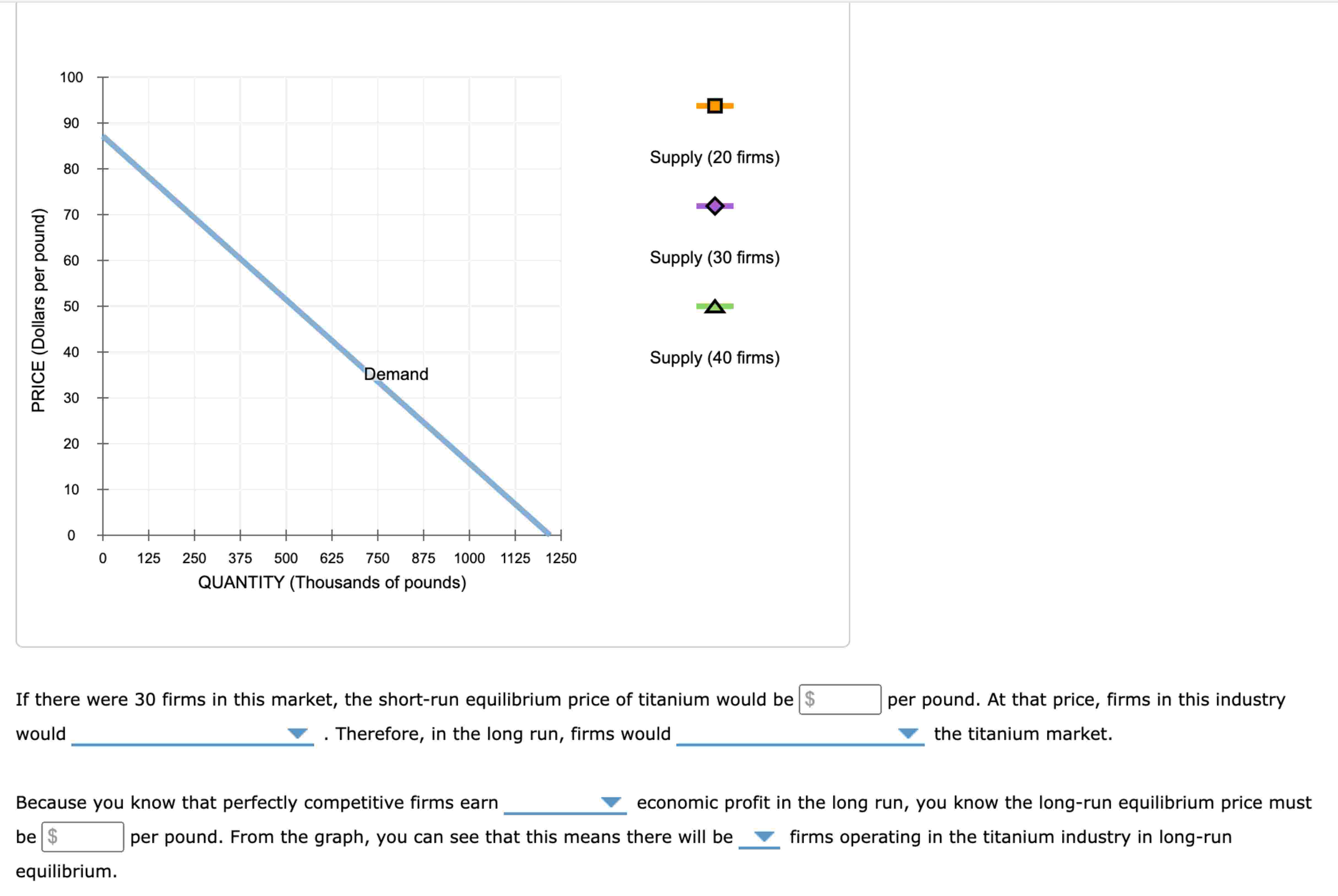

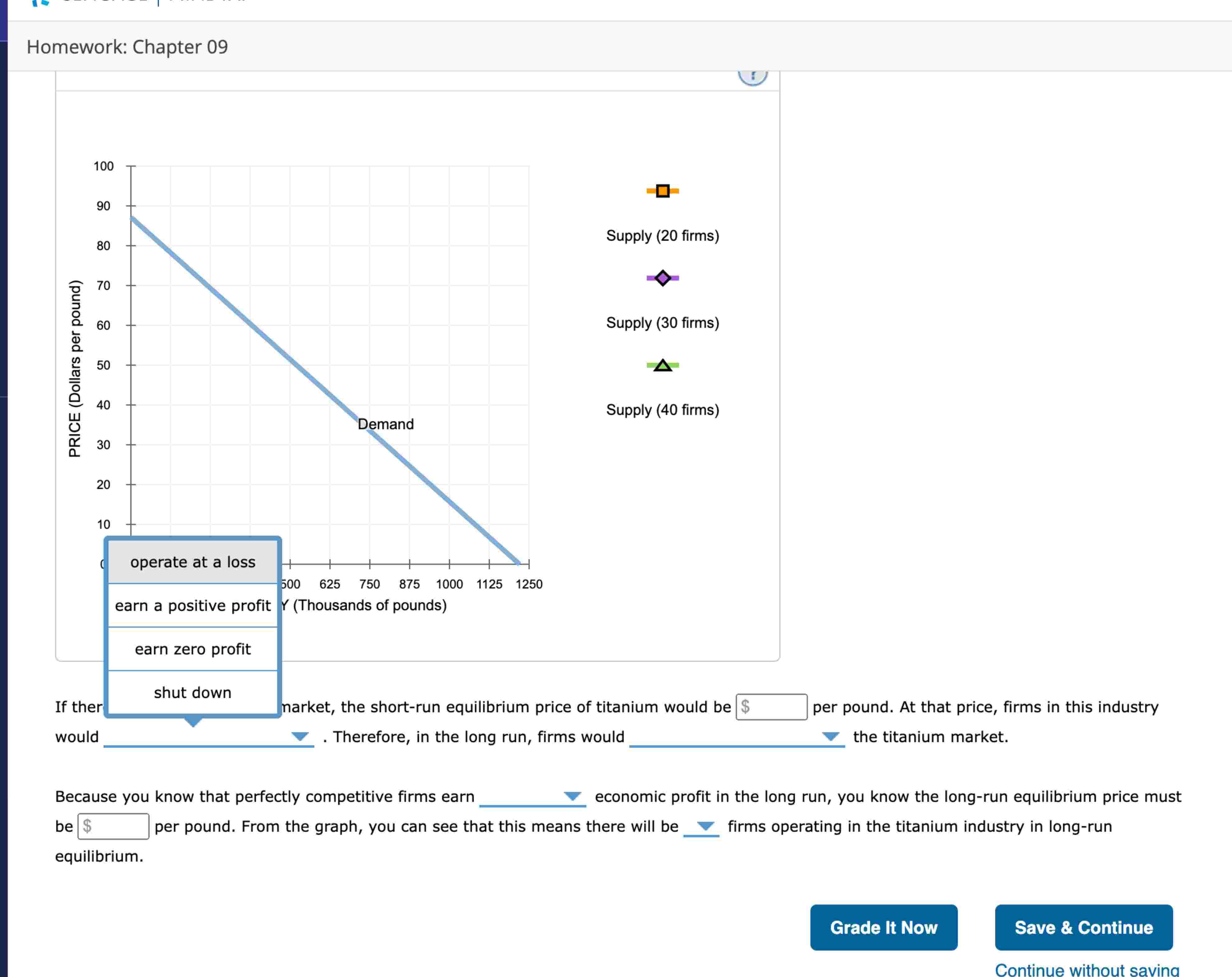

5. Short-run supply and long-run equilibrium Consider the perfectly competitive market for titanium. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. The following diagram shows the market demand for titanium. Use the orange points (square symbol) to plot the initial short-run industry supply curve when there are 20 firms in the market. (Hint: You can disregard the portion of the supply curve that corresponds to prices where there is no output, since this is the industry supply curve.) Next, use the purple points (diamond symbol) to plot the short-run industry supply curve when there are 30 firms. Finally, use the green points (triangle symbol) to plot the short-run industry supply curve when there are 40 firms. Supply (20 firms) Supply (30 firms) Supply (40 firms) If there were 30 firms in this market, the short-run equilibrium price of titanium would be ? per pound. At that price, firms in this industry would = . Therefore, in the long run, firms would qquad the titanium market. Because you know that perfectly competitive firms earn economic profit in the long run, you know the long-run equilibrium price must be per pound. From the graph, you can see that this means there will be qquad firms operating in the titanium industry in long-run equilibrium. Homework: Chapter 09 If ther shut down narket, the short-run equilibrium price of titanium would be per pound. At that price, firms in this industry would . Therefore, in the long run, firms would the titanium market. Because you know that perfectly competitive firms earn economic profit in the long run, you know the long-run equilibrium price must be per pound. From the graph, you can see that this means there will be firms operating in the titanium industry in long-run equilibrium. Last 3 drop-down options: 1. exit, enter, neither 2. negative, positive, 0 3. 20, 30, 40