Home /

Expert Answers /

Statistics and Probability /

the-random-variables-x-and-y-are-said-to-have-a-bivariate-normal-distribution-if-their-joint-density-pa190

(Solved): The random variables x and Y are said to have a bivariate normal distribution if their joint density ...

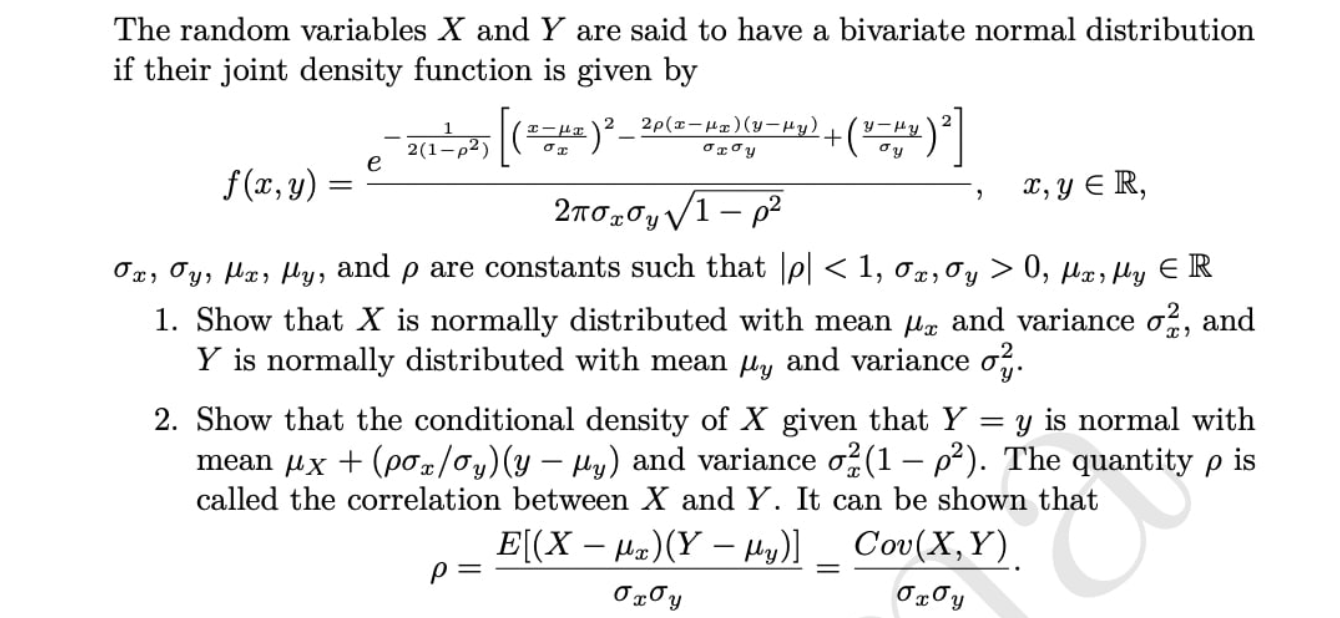

The random variables x and Y are said to have a bivariate normal distribution

if their joint density function is given by

f(x,y)=(e^(-(1)/(2(1-\rho ^(2)))[((x-\mu _(x))/(\sigma _(x)))^(2)-(2\rho (x-\mu _(x))(y-\mu _(y)))/(\sigma _(x)\sigma _(y))+((y-\mu _(y))/(\sigma _(y)))^(2)]))/(2\pi \sigma _(x)\sigma _(y)\sqrt(1-\rho ^(2))),x,yinR

\sigma _(x),\sigma _(y),\mu _(x),\mu _(y), and \rho are constants such that |\rho |<1,\sigma _(x),\sigma _(y)>0,\mu _(x),\mu _(y)inR

Show that x is normally distributed with mean \mu _(x) and variance \sigma _(x)^(2), and

Y is normally distributed with mean \mu _(y) and variance \sigma _(y)^(2).

Show that the conditional density of x given that Y=y is normal with

mean \mu _(x)+(\rho (\sigma _(x))/(\sigma _(y)))(y-\mu _(y)) and variance \sigma _(x)^(2)(1-\rho ^(2)). The quantity \rho is

called the correlation between x and Y. It can be shown that

\rho =(E[(x-\mu _(x))(Y-\mu _(y))])/(\sigma _(x)\sigma _(y))=(Cov(x,Y))/(\sigma _(x)\sigma _(y)).